How Outscourcing Helps in Mitigating Payroll Fraud Risks

Summary:

Payroll fraud remains a serious operational risk for organizations of all sizes. Weak controls, manual processes, and limited oversight make payroll vulnerable to errors and misuse. This blog explains how modern payroll outsourcing strengthens internal controls, improves accuracy, and reduces fraud exposure. It also explores how Outsourcing 3.0 embeds risk mitigation directly into payroll delivery, helping organizations operate with greater confidence and control.

Payroll is one of the most sensitive financial functions in any organization. It affects employee trust, regulatory compliance, and direct cash outflows. At the same time, it is one of the most exposed areas for fraud when controls are weak or processes depend heavily on manual effort.

As payroll volumes grow and timelines tighten, many organizations find it difficult to rely on traditional in-house models alone. This is where Outsourcing 3.0, the most sustainable evolution of outsourcing, plays a critical role. It helps businesses prevent payroll fraud while improving accuracy and operational control.

This blog looks at why payroll fraud occurs, why in-house payroll teams often struggle to stop it, and how outsourcing reduces risk through stronger processes, technology, and governance.

Understanding Payroll Fraud and Its Impact

Payroll fraud occurs when payroll processes are manipulated for personal gain or due to a lack of oversight. Common examples include ghost employees, inflated work hours, unauthorized pay changes, and duplicate or incorrect payments.

The impact goes far beyond financial loss. Payroll fraud can result in compliance violations, failed audits, employee distrust, and reputational damage. Even small discrepancies, when repeated over time, can turn into significant risk.

Outsourcing 3.0 addresses today’s offshoring challenges head-on.

QX is leading this shift by helping firms close payroll risk gaps and do much more through a secure, structured delivery model. Want to learn more?

Why In-House Payroll Alone Struggles to Prevent Payroll Fraud

Many organizations manage payroll internally with limited resources and overlapping responsibilities. While this may work at a smaller scale, risks rise quickly as complexity increases.

One of the most common issues is the lack of segregation of duties. In-house teams often have the same individuals handling data entry, payroll processing, and approvals. This makes it easier for errors or misconduct to go unnoticed. Reviews may also become informal or rushed, especially during peak periods.

Another challenge is heavy reliance on manual processes. Spreadsheet-based workflows and manual checks depend on constant attention and experience. Over time, fatigue and workload pressure reduce the effectiveness of these controls.

In addition, many in-house teams lack consistent audit trails and monitoring tools. Without structured logging or automated alerts, unusual changes may only surface after payments are already made.

Payroll fraud is not a rare exception. According to the Association of Certified Fraud Examiners, payroll fraud accounts for 27% of all occupational fraud cases, with average losses of $100,000 per incident. This level of exposure is difficult for most in-house payroll teams to manage on their own.

Outsourcing 3.0: A Stronger Framework for Reducing Risk

Outsourcing has evolved far beyond basic task delegation. Outsourcing 3.0 brings together trained teams, standardized processes, automation, and built-in governance.

Rather than relying on individual effort, modern outsourcing embeds controls directly into workflows. Approvals are enforced consistently. Access is restricted by role. All changes are logged, tracked, and reviewed.

This approach creates a controlled environment where payroll activity is transparent, repeatable, and continuously monitored. It reduces dependence on single points of failure and strengthens accountability across every step of payroll processing.

“Outsourcing 3.0 is less about moving work offshore and more about redesigning operating models. It reduces risk, strengthens controls, and creates transparency at scale. In today’s environment, risk mitigation must be built into the delivery model. There is no other way.”

Sagar Ahuja, CEO, QX Accounting Services

According to Statista, nearly 83% of companies that adopted payroll outsourcing reported improved fraud detection capabilities, reinforcing the value of structured controls and independent oversight.

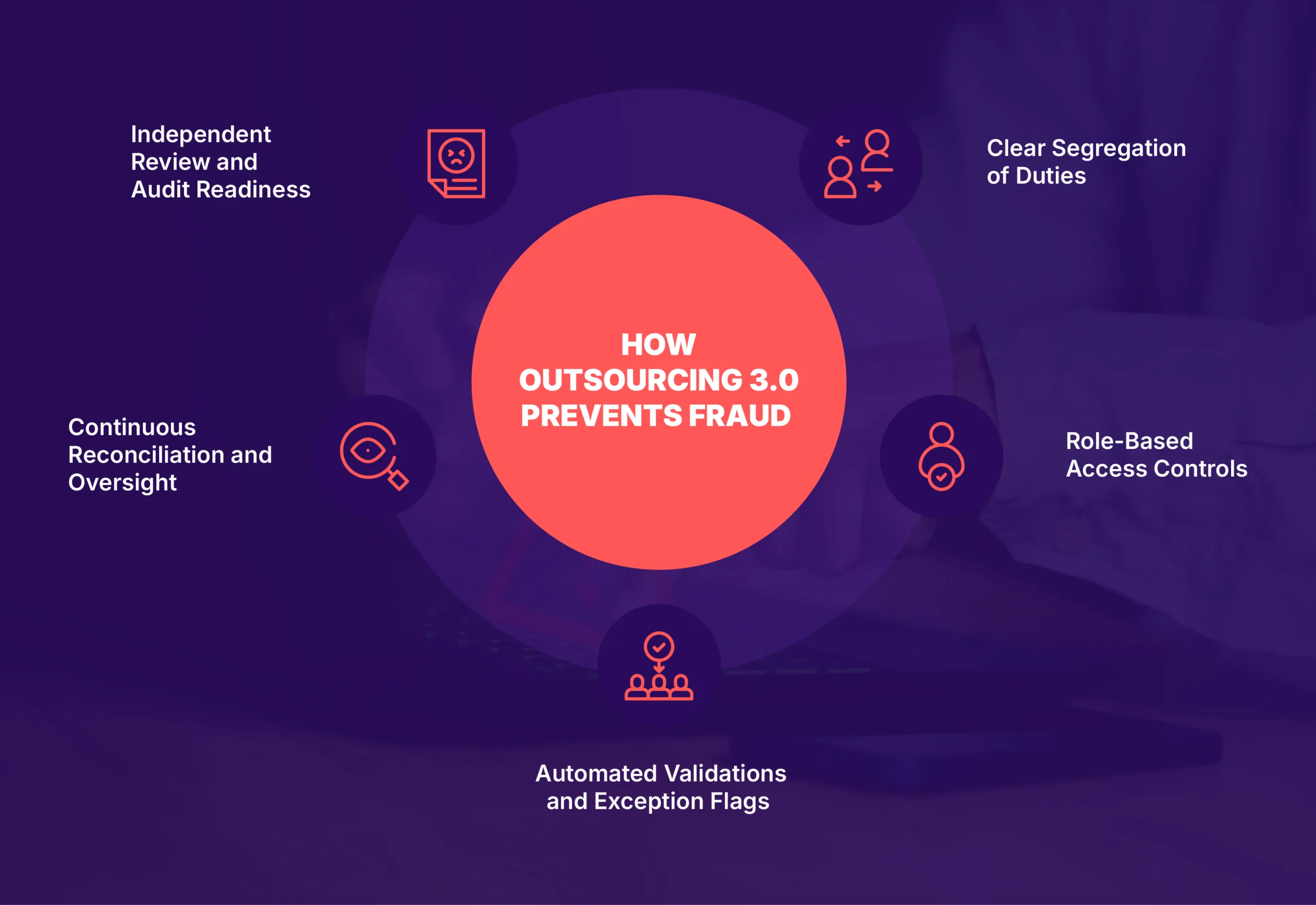

How Outsourcing 3.0 Helps Prevent Payroll Fraud

1. Clear Segregation of Duties

Outsourced payroll models separate data entry, processing, and approvals across defined roles. This reduces the risk of unauthorized changes and ensures no single individual controls the full process.

2. Role-Based Access Controls

Outsourcing environments enforce strict access permissions. Only authorized users can view or modify sensitive payroll data, limiting exposure and reducing misuse risk.

3. Automated Validations and Exception Flags

Automation applies consistent checks across payroll runs. Unusual pay changes, duplicate entries, or missing approvals are flagged early, before payments are released.

4. Continuous Reconciliation and Oversight

Payroll data is regularly reconciled with general ledger and bank records. This ongoing monitoring helps identify discrepancies quickly and prevents small issues from escalating.

5. Independent Review and Audit Readiness

Outsourced teams maintain structured documentation, logs, and review layers. This independent oversight improves audit outcomes and strengthens overall control integrity.

The Broader Payoff: Compliance, Efficiency, and Trust

Beyond fraud prevention, Outsourcing 3.0 strengthens payroll operations in measurable ways. Stronger compliance is one of the benefits. This mainly happens because processes are aligned with regulatory requirements and updated regularly. With automation replacing manual intervention, error rates drop significantly across the payroll process.

Efficiency also improves. Payroll cycles become more predictable, and internal finance teams spend less time on rework and exception handling. This allows them to focus on higher-value analysis and planning.

Most importantly, outsourcing helps build trust across the organization. Employees are paid accurately and on time, reinforcing confidence in payroll operations. Leadership gains clearer visibility into payroll activity, while auditors encounter structured controls and documented processes instead of reactive fixes.

Final Thoughts

Payroll fraud rarely results from a single bad decision. It typically stems from weak controls, limited visibility, and an overreliance on manual processes.

Modern outsourcing addresses these gaps by combining structured workflows, automation, and independent oversight. When implemented correctly, it acts as a preventive control rather than just a processing solution.

Partners like QX, operating within an Outsourcing 3.0 framework, help organizations reduce payroll risk while improving accuracy, compliance, and operational confidence.

If payroll risk is keeping you up at night, it may be time to rethink how payroll is delivered. Connect with QX to explore a safer, more controlled approach.

Cora Vollmar

Cora Vollmar is a seasoned professional with over 20 years of experience in accounting, operations, talent management, and business development. Her career began in the construction sector, where she quickly established herself as a leader, achieving triple-digit growth with her CPA team. Cora’s extensive experience includes recruiting for finance and accounting roles, developing innovative STEM-driven solutions to address the U.S. talent deficit, and leading capacity panel discussions across the country.

Recognized as a member of one of America’s fastest-growing construction companies by the Inc. 5000 list for three consecutive years, Cora’s expertise and passion for growth are evident in every aspect of her work. She brings a wealth of knowledge and a dynamic approach to QX Global Group, where she is poised to make a significant impact.

When she’s not working, Cora is an avid traveler with a love for exploring new cultures. She has visited Canada, Mexico, the Caribbean, Europe, the UK, and Central America, with plans to visit Ireland in 2025.

Unauthorized copying or plagiarism of our content is a violation of intellectual property rights. We take such matters seriously and will pursue legal action to protect our original work. Anyone found engaging in such activities will be held accountable under applicable laws.

Don't forget to share this post!

Our Latest Insights

Let’s Work Together

Explore outsourcing solutions, request a free trial or discuss your practice’s needs with our expert consultants.

Get Your ROI Estimate

Get Your ROI Estimate